Sustainability Report Quality: Media and Shareholder Effect

##plugins.themes.academic_pro.article.sidebar##

Downloads

##plugins.themes.academic_pro.article.main##

Abstract

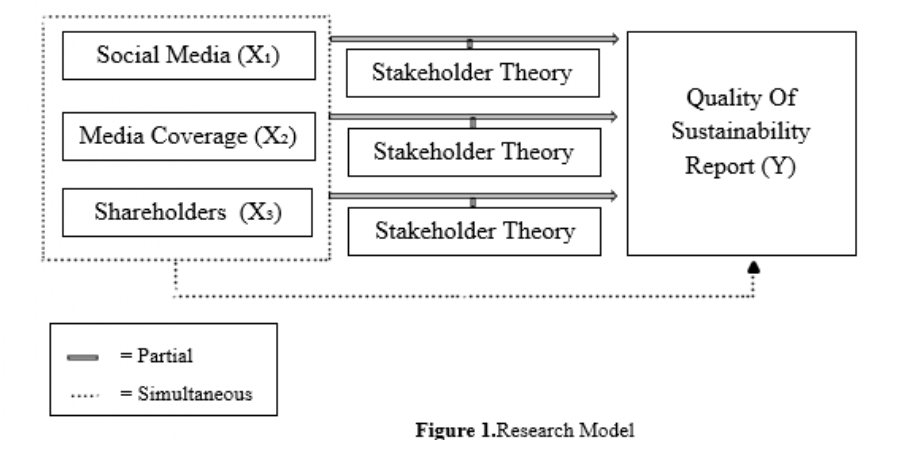

The research objective is to examine the effect of social media, media coverage, shareholders on the quality of sustainability reports. Measurement of social media variables from the number of likes, comments, tweets on facebook, instagram, twitter. media coverage from the number of negative issues on the detik and kompas websites. shareholders from the largest percentage of share ownership. quality of sustainability reports through the 2016 GRI index. The research population is public companies in the Consumer Non Cyclicals sector, using purposive sampling technique in determining the sample obtained 53 companies. Technical data analysis using multiple linear regression. The results of the study are social media, media coverage, shareholders have no effect on the quality of sustainability reports. the findings show limited utilization of social media by 53 sample companies for sustainability, so that differences in research samples can be the cause of different influences with previous studies.

##plugins.themes.academic_pro.article.details##

This work is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.

LPPM Politeknik Piksi Ganesha Indonesia

References

Clarkson, M. E. (1995). A stakeholder framework for analyzing and evaluating corporate social performance. Academy of Management Review, 20(1), 92–117.

Fernandez-Feijoo, B., Romero, S., & Ruiz, S. (2014). Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. Journal of Business Ethics, 122, 53–63.

Ghozali I. (2016). Aplikasi Analisis Multivariete Dengan Program IBM SPSS 23. Badan Penerbit Universitas Diponegoro Press.

Hamid, S., Ijab, M. T., Sulaiman, H., Md. Anwar, R., & Norman, A. A. (2017). Social media for environmental sustainability awareness in higher education. International Journal of Sustainability in Higher Education, 18(4), 474–491.

Hamudiana, A., & Achmad, T. (2017). Pengaruh tekanan stakeholder terhadap transparansi laporan keberlanjutan perusahaan-perusahaan di Indonesia. Diponegoro Journal of Accounting, 6(4), 226–236.

Lodhia, S., Kaur, A., & Stone, G. (2020). The use of social media as a legitimation tool for sustainability reporting: A study of the top 50 Australian Stock Exchange (ASX) listed companies. Meditari Accountancy Research, 28(4), 613–632.

Manetti, G., & Bellucci, M. (2016). The use of social media to engage stakeholders in sustainability reporting. Accounting, Auditing and Accountability Journal, 29(6), 985–1011. https://doi.org/10.1108/AAAJ-08-2014-1797

Nazari, J. A., Herremans, I. M., & Warsame, H. A. (2015). Sustainability reporting: External motivators and internal facilitators. Corporate Governance, 15(3), 375–390.

Nugraheni, G. K., Widyastuti, S., & Fahria, R. (2021). Pengaruh Tata Kelola Perusahaan, Ukuran Perusahaan, dan Keterbukaan Massa Terhadap Pengungkapan Informasi Lingkungan. Infestasi, 17(1), 45–54.

Qisthi, F., & Fitri, M. (2020). Pengaruh Keterlibatan Pemangku Kepentingan terhadap Pengungkapan Laporan Keberlanjutan Berdasarkan Global Reporting Initiative (GRI) G4. Jurnal Ilmiah Mahasiswa Ekonomi Akuntansi (JIMEKA), 5(4), 469–484.

Rahmansyah, A., Mulyany, R., & Geumpana, T. A. (2023). Using Social Media as A Legitimation Tool in Sustainability Reporting: Evidence from SOEs Listed on the Indonesia Stock Exchange. Jurnal Dinamika Akuntansi Dan Bisnis, 10(2), 265–284.

Ruhiyat, E., Hakim, D. R., & Handy, I. (2022). Does Stakeholder Pressure Determine Sustainability Reporting Disclosure?: Evidence From High-Level Governance Companies. Jurnal Reviu Akuntansi Dan Keuangan, 12(2), 432–453.

Sari, P. N., & Nurkhin, A. (2020). Determinan Kualitas Sustainability Report Perusahaan LQ45 Tahun 2017 dan 2018. Economic Education Analysis Journal, 3(1).

Solikhah, B., & Maulina, U. (2021). Factors influencing environment disclosure quality and the moderating role of corporate governance. Cogent Business & Management, 8(1), 1876543.

Sriningsih, S., & Wahyuningrum, I. F. S. (2022). Pengaruh Comprehensive Stakeholder Pressure dan Good Corporate Governance terhadap Kualitas Sustainability Report. Owner: Riset Dan Jurnal Akuntansi, 6(1), 813–827.

Sugiyono. (2018). Metode penelitian kuantitatif (Cet 1). Alfabeta.

Suharyani, R., Ulum, I., & Jati, A. W. (2019). Pengaruh Tekanan Stakeholder dan Corporate Governance terhadap Kualitas Sustainability Report. Jurnal Akademi Akuntansi, 2(1).

Tizmi, S., Luthan, E., & Rahman, A. (2022). Kualitas Laporan Keberlanjutan: Eksistensi dari Media dan Industri. E-Jurnal Akuntansi, 32(2), 3750.

Trianaputri, A. R., & Djakman, C. D. (2019). Quality of sustainability disclosure among the ASEAN-5 countries and the role of stakeholders. Jurnal Akuntansi Dan Keuangan Indonesia, 16(2), 4.

Yosua, A., & Tundjung, H. (2022). Pengaruh Pemangku Kepentingan Dan Pemegang Saham Terhadap Kualitas Laporan Berkelanjutan. Jurnal Paradigma Akuntansi, 4(3), 1312–1321.

Zakaria, D. K. P., Hastuti, S., & Widiastuti, S. W. (2023). Pengaruh Liputan Media, Sensitivitas Lingkungan, Environmental Management System, dan Kedekatan Konsumen terhadap Pengungkapan Lingkungan. Nominal Barometer Riset Akuntansi Dan Manajemen, 12(1), 59–71.